The US Federal Reserve has been tapering off its pandemic-era economic stimulus since the beginning of 2022. That taper coincided with declines in the prices of flagship digital assets BTC and ETH, and some tremors in the stock market as investors adjust. Now, though, it seems the problems may be more serious. The Fed stopped adding new bonds to its balance sheet in March this year, and since then, the financial outlook has become significantly bleaker. A recession in the US economy is now thought likely by several credible commentators, with obvious global knock-on effects.

Inflation has risen, touching 40-year highs in May 2022 and spending several months above 8%, more than double its long-term average — and four times the Fed’s “long-term goal of 2%”. Yields remain low, with neither trend showing signs of abating. In what Forbes’ Adam Strauss calls “an era of low-yield bonds”, and with the Fed likely to raise the interest rate again, there’s a good chance that the US economy could slip into recession.

Concerns aren’t abstract: the stock market began the year with its worst quarter since the pandemic-induced slump two years ago.

As the economy shrank 1.4% , investors responded. Morgan Stanley analyst Mike Wilson warned of an “especially vicious” stock selloff, and suggested we could be entering a period in which “nothing works” for investors, including defensives.

To understand what’s happening, let’s first look at what the Fed is doing.

Raising interest rates

The Federal Reserve is no longer pumping money into the economy via bond purchases; it’s also increasing the interest rate. Interest rates are a traditional lever for the Fed to manage the pace of the economy, but the speed at which it’s changing is unusual in the modern era. Usually the Fed moves the inflation rate a quarter of a percentage point at a time. The Fed began by raising the rate 0.5%. That doesn’t sound like much, but to people familiar with the territory it’s a big enough jump to generate a lot of commentary: it’s the biggest hike in over 20 years. The target is rising inflation, currently running at a 40-year high.

The Fed is also expected to make similar large raises in the future in a bid to “restore price stability”, in the words of chairman Jerome Powell. At the time Powell made those comments, May 4 this year, it seemed the Fed didn’t intend to go higher than this: “Seventy-five basis points is not something the committee is actively considering”. However, the Fed made a 0.75% raise on June 15, its most aggressive move since 1994, and there may be more on the horizon. In a press conference following the June 15 meeting of the Fed, Chair Powell said “the median projection for the appropriate level of the federal funds rate is 3.4% at the end of this year, 1.5 percentage points higher than projected in March and 0.9 percentage point above the median estimate of its longer-run value”.

However, Powell continued, “the median projection rises further to 3.8% at the end of next year and declines to 3.4% in 2024, still above the median longer-run value. Of course, these projections do not represent a Committee plan or decision, and no one knows with any certainty where the economy will be a year or more from now”. Such a change would put the federal rate at a level not seen since January of 2008.

Rising inflation

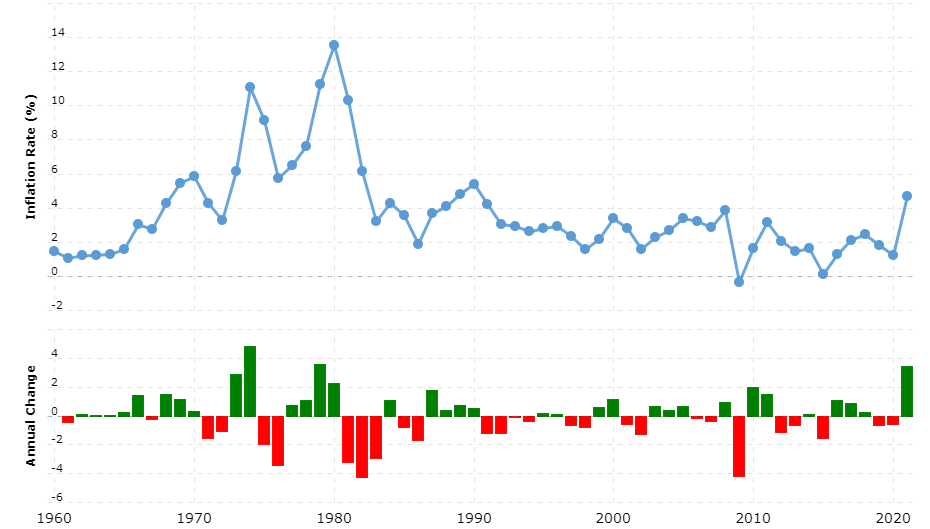

Rising inflation remains a serious problem in the US economy. While Powell’s May speech addressed the concerns of low-income citizens, inflation has deleterious effects on investment income and consumes savings — including both personal savings and the cash component of corporate treasuries. The US inflation rate hasn’t risen above 4% this millennium, including a drop to an unprecedented -0.36% rate in 2009.

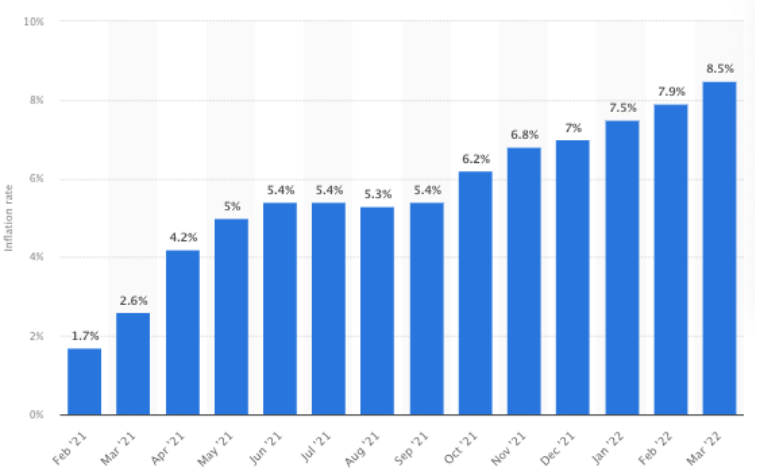

However, it’s now at more than double the peaks of the last 20 years and trending up:

Higher oil and fuel prices are expected to follow the conflict in Ukraine, meaning pressure on household spending and business operations — and concomitant pressure on earnings as aggregate demand is depressed.

In particular, some parts of the economy are experiencing a rate of inflation not shown on an aggregate graph. In the US, the general rate of inflation is currently 8.6%; however, food (10.1%), electricity (12.0%), and utilities (30.2%) are all experiencing inflation well above this, and prices directly linked to the prices of refined oil products are suffering most of all. Air fares are subject to 37% inflation; gasoline prices are at nearly 50% inflation.

Tapering investment support

The Federal Reserve has been buying Federal securities and agency mortgage-backed securities to support the US economy’s credit flows during the pandemic. Late last year, Powell announced that it would begin cutting back on these purchases, shaving off $15 billion each month from the $120 billion a month the Fed was then buying: $10 billion in Treasury and $5 billion in mortgage-backed securities. This process is now complete, and the Fed has stopped buying altogether.

“Our baseline expectation is that supply chain bottlenecks and shortages will persist well into next year”, announced Powell in November of last year — by which time, the Federal reserve had bought $4 trillion in US Treasury and other securities. Powell added that the Fed expected to see “elevated inflation as well”, though it now seems likely that its expectations were too conservative.

This QA (Quantitative Easing) approach to supporting the economy depressed earnings from the bond market by driving up the prices of securities. In December, the Fed decided to accelerate tapering and cut $20 billion from its monthly purchase .

The Fed held off intervening as inflation rose, out of a desire not to impede America’s incipient recovery. With inflation increasingly a concern, the taper accelerated. The Fed initially planned to stop buying bonds, but the current plan calls for even more drastic measures: there will also be bond sales, expected to account for $95 billion per month.

The plan outlined in May this year will see the Fed allow a capped level of proceeds from maturing bonds to roll off each month while reinvesting the rest.

Starting June 1, $30 billion of Treasury bonds and $17.5 billion on mortgage-backed securities began rolling off. After three months, the cap for Treasury bonds will increase to $60 billion and that for mortgages to $35 billion.

How investors are responding

Faced with these factors, investors are moving away from riskier stocks. (This might go some way to explaining the recent downturn in tech stocks.) Traditionally, rising inflation points investors and money managers toward defensive value stocks rather than riskier, potentially more rewarding investments such as high-growth tech companies.

However, this isn’t as easy for modern investors as it could be. Low earnings from all investments mean that many investors are struggling to retain the value of their investments; the same inflation that drives them to defensive investments also destroys the value of those investments, because earnings are so historically low. Yet, with inflation so high, cash has little appeal.

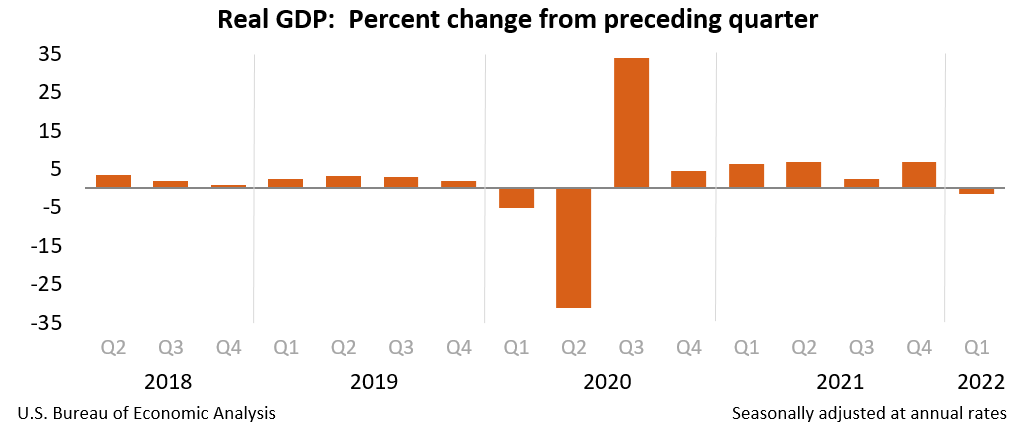

The result can be the situation outlined as a possibility by Mike Wilson earlier in this post: “nothing works”. The US economy contracted in Q1 2022, meaning that whether we’re using the word “recession” or not is really a question of degree.

The S&P adds heft to the possibility of a real recession, showing the worst first-half performance since the early 1970s. Wilson predicts a further 8% drop in the coming months, and warns that “If there’s a true growth scare with recession probabilities rising materially,” the S&P could fall twice that far. A plunge like that would take the index to 3,460 points, which would line up with the index’s pre-pandemic highs—“where a lot of stocks have already ventured”, as Wilson notes. (At the time of writing, the S&P stands at 3,739.88, having fallen over 2% today.) Of the US’s three major stock indexes, only the blue-chip Dow showed some growth.

“The market’s struggling to find direction”, Megan Horneman, chief investment officer at Verdence Capital Advisors in Hunt Valley, Maryland, told Reuters. “We had disappointing data, and the markets are waiting for earnings season, when we’ll get more clarity” on future earnings and any economic slowdown.

Does all this add up to recession?

Not necessarily. So far we’ve heard just one side of the argument. Powell observed in his May statement that the economy “edged down in the first quarter” but noted that “household spending and business fixed investment remained strong.” However, household spending is an open question: rising wages and demand for labor helped Q2 2022 start stronger than expected, but skyrocketing fuel prices and a looming food price crisis will tend to reinforce each other’s effects and make a big dent in household incomes.

Bank of America economist Ethan Harris noted that “recession risks are low now, but elevated in 2023,” and warned that continuing inflation could tip the Fed’s hand, obliging Powell to raise interest rates “until it hurts” and eat into corporate profits; the result could be a slew of layoffs that impede recovery and depress household and business spending. Arguably this has begun; digital assets firms shed staff at the end of May in response to falling prices and yields, with Coinbase dropping 18% of its total staff.

Meanwhile, Goldman Sachs economist Jan Hatzius told clients that “a recession is not inevitable”, placing the likelihood of a full-blown slump at 15% over the next year and 35% over the next two years.

Hatzius argues that typically recessionary factors might play out differently in today’s landscape. An overheated labor market and the highest inflation in decades are headwinds, but the Covid stimulus has not ceased to affect the US economy. In particular it helped SMBs and heavily-indebted companies into a historically strong position against the higher interest rates to which they are traditionally vulnerable. This could help reduce the effects of tapering Fed support and high interest.

Unknowns ahead

Hatzius also points to several unknowns, with the most imminent concern being supply-side problems as a hangover from the pandemic. If these can be solved relatively quickly, goods prices could fall and take inflation down with them. However, the continued effects of the pandemic and the war in Ukraine both pose serious risks to this assumption. Higher fuel and thus transportation prices, a squeeze on food supplies, or disrupted global trade could all slow a return to normal and “make it harder to calm inflation”.

Conclusion

The US isn’t the only world economy facing headwinds. The world could be facing a global downturn as deglobalization, higher fuel prices and inflation collide with the withdrawal of Covid stimulus. However, such an outcome is, in Hatzius’ words, “not inevitable”. Investors are likely to be seeking safe-haven investments which also offer a yield above inflation, which may partly explain a significant rally in BTC prices following the Fed’s announcement. With gold underwater compared to inflation, we’d normally expect to see more activity in traditional digital assets, EFTs, and alternative investments; recent downward trends in BTC and ETH suggest otherwise, suggesting yet more unpredictability.